Oil crisis aside, weather has now become a near constant feature in the food price index over the past year

The price of food is on a tear around the world. Global food prices are now 28% higher than they were at this time last year, and almost 40% higher than prices in November 2019. According to the latest update to the FAO’s Food Price Index (FFPI), released on December 2, the latest increase marks the fourth consecutive rise in the index and puts it at the highest level in over a decade.

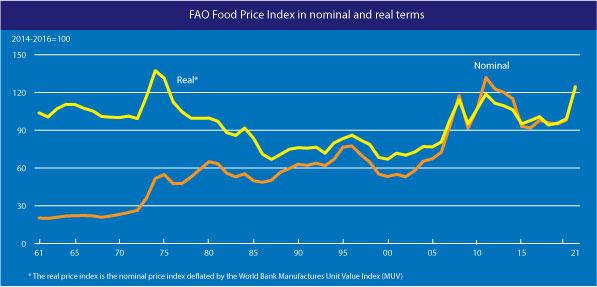

The FFPI, however, doesn’t give the full story of how grievous the unraveling of food prices actually is. The FFPI has been formulated to convert actual price changes in a basket of food commodities, including cereals, vegetable oils, meats and sugars, into an index that is charted monthly. Effectively, this formulation generates a nominal price index, which can be used to track monthly changes in price, relative to baseline average of prices from 2014-16. While this is a convenient standard to track short-term trends, it does not reflect the double whammy of inflation or the real price of food.

When adjusted for inflation, the implications of the FFPI chart take on more daunting implications. According to independent analysis of real and nominal prices, the real price of food had shot past the 2011 peak back in August of this year, after which prices have continued to climb. In reality, prices are currently approaching levels not seen in almost 50 years.

Déjà vu in real time

Real prices this high were last seen in the early 1970s, when a rapid escalation in food prices finally climaxed with the 1973 oil crisis. Oil prices quadrupled practically overnight as the geopolitical turmoil caused by the Yom Kippur war spilled over into trade and global energy security. With oil prices remaining high for years, global food prices, too, retreated to pre-1972 levels only after 1976.

Incidentally, the parallels between the current situation and the one in the early 70s are hard to miss. While the primary trigger for the oil crisis (this time, the global pandemic driven supply shock), is vastly different, the effect on global markets has been markedly similar. Following the massive crash of crude oil after global lockdowns were enforced, economic recovery around the world comes with a shadow fraught with energy economics. As demand grew in 2021, crude oil supplies have remained tightly controlled amid continued uncertainties surrounding COVID.

The supply shock was recently felt across the world as oil prices raced upward August through September of this year. Prices are only now receding tentatively following output increases from oil-producing countries and strategic reserve releases from several countries. However, prices remain around 30% higher than the beginning of the year, with looming fears of a spike in COVID cases caused by the Omicron variant bringing a fresh layer of uncertainty to the phased plan to increase oil outputs.

As if things were not tenuous enough, there is also the simmering risk of military conflicts breaking out in the Middle East and the Russia-Ukraine border, which could have a protracted effect on global energy markets.

While disruptions in the global oil markets are strong indicators of spikes in food price, the two are not absolutely correlated. A testament to this is the oil crisis of 1979, during which food prices actually fell despite pressures on the global oil supply chain.

The compounding effect of climate

The food price spike in 1973 did not happen suddenly. In fact, prices were already on a steep incline for over a year before peaking with the energy crisis. According to FAO’s 1973 Status of Food and Agriculture report, drought was the primary cause for a decline in world food production for the first time since the Second World War in 1972, just as prices started creeping up.

The current spike in global food prices is also embedded with deep imprints of extreme weather. Weather has become a near constant feature in FAO’s FFPI updates over the past year as inclement weather around the world has added to the supply side strains caused by the pandemic.

A year of drought, flood and frost in Brazil, along with increasing pressures to increase ethanol supplies, has seen prices of coffee and sugar, most prominently, shoot up. Elsewhere in South and Latin America, too, food prices have been climbing rapidly as crop losses due to poor weather compounds disruptions in food supply chains. China’s monsoon rains brought historic levels of flooding to the central province of Henan and affected crop production and livestock in the. The summer was marked by a protracted heatwave and dry spell in North America, which has had an adverse effect on the output of farms in the agricultural belts of Canada and the US. Huge crop losses were reported from Europe, too, where a hot summer was accompanied by spells of heavy rains in Germany, Belgium and UK. A long-protracted drought in Eastern Africa has sparked fears of severe malnutrition in the region, while massive hikes in food prices have sparked riots in several parts of North Africa and the Middle East. India’s monsoon, which swung between extreme rain and extreme dryness between June and October, saw crops affected in over 5 million hectares.

The imprint of extreme weather and climate change in the current price trend is clearly analogous to the price spike of the early 1970s, except unlike before, extreme weather is now increasingly becoming an ‘all the time, everywhere’ kind of phenomenon. The real price of food has been on a prolonged upward trend since 2000, in lock-step with the increases in incidence of climate- and weather-related disasters as recorded by the FAO.

Unfortunately, the upward trend with respect to extreme weather is not surprising or startling. Several reports, including the IPCC Special Report on Climate Change and Land, have already foretold the story of how climate change is likely to create both short-term and long-term pressures on food availability. While increasing frequency of extreme weather creates upward pressures on food prices, sustained yield losses are projected in major cereal crops, particularly maize and wheat, even as demand keeps ticking up. Global stocks of cereals could be offering the first signs of such an eventuality. The global cereal stock looks set to record its fifth straight year of reductions after several successive years of growth since the early 2000s.

TOPping out: India’s food inflation problem looks set to worsen

Weeks before India’s Union minister of agriculture and farmers’ welfare Narendra Singh Tomar apprised the Lok Sabha of the crop damage during the 2021 monsoon, the Ministry of statistics revealed that India had recorded its highest ever Consumer Food Price Index in October 2021, marking the end to a three-month stagnation in food prices. According to the CFPI, food prices in India are 20% more expensive than they were in October 2018.

The short-term trend reversal came primarily as a reflection of the escalation in global prices of edible oils and fats, which in October 2021 was 56% more expensive than three years ago. Interestingly, after two successive years of high inflation in vegetables in September and October, the prices of vegetables saw a net reduction this year compared to the same period in 2020, effectively bringing average prices to 2019 levels.

The respite in vegetable prices, however, is likely to be temporary. Vegetable prices, according to the RBI, are correlated the closest with weather in the basket of commodities used to determine food inflation. The year-on-year reduction in vegetable prices in India, although, does not fully capture the effect of heavy rainfall in September, the extension of monsoon rains in October or the spells of heavy rainfall that have hit several parts of the country in November. As per the RBI’s assessment, the impacts of weather on vegetable prices are often seen in the food price index with a lag and can stretch on for months. A large majority of the double-digit inflation instances since 1956 have had clear imprints of extreme weather and climate affecting the supplies of food and driving up prices.

From October to December 2021, close to 70% of the country saw rainfall excesses of over 20%. Even as October inflation figures were being published by the government, extreme rain and crop damages drove prices of tomatoes over Rs100/kg in several key tomato-producing regions in the country, including Andhra Pradesh, Karnataka, Maharashtra and Uttar Pradesh, reflecting a nearly 2,000% increase in just a couple of months. India’s two other vegetable staples—onions and potatoes— while more stable than tomatoes, also saw prices increasing in October before coming down again in November, in part due to the deployment of buffers. The prices of both, however, still remain about 20% above September rates in India’s major agricultural markets.

The effects of the unusually wet spells in November and early December in several parts of the country, analysts believe, will likely keep vegetable prices high for a few more months. While tomato prices are expected to come down to under Rs50/kg by January 2022, an upswing in the prices of predominantly winter crops onions and potatoes could be in the offing as heavy rainfall and reported waterlogging from around the country could translate to upward pressures on price in the coming months.

The spikes in food and vegetable prices, particularly over the past three years hold a pertinent warning. While price rise due to extreme weather events are often termed transitory, the effects could drive prices to multi-decade cumulative levels. The costs of climate change are likely to be staggered and incremental rather than momentous. Food price trends, however, show the world is already on the path to steep but sustained hikes. It is only a matter of time before the effects on food security become hard to ignore.

About The Author

You may also like

Climate Talks in 2025: Converging Crises, Rising Stakes, and Diminished Returns

Can biochar be India’s missing link to carbon capture?

India’s coal heartland is powering down, with no safety net

Trump’s trade war revives a vital old question: Can the Global South go its own way?

From waste to resource: Can urban India turn the tide on its water crisis?