Carbon capture and removal: Not all it is cracked up to be

The IPCC says the world will need carbon capture and removal in the long run, but a measured approach to CCUS will ensure current bloated costs, and tall claims made by private players are eventually kept in check

While a rapid expansion of carbon capture and removal capacities is required in order to lower atmospheric carbon concentrations, it is feared that expanding CCS would in effect prolong the use of fossil fuels. Photo: Climeworks

India’s climate action plan looks set to have a new addition—carbon removal. The Indian government has been quietly exploring the carbon removal option since the PM’s net zero announcement at COP26 in November last year. The first noticeable move in this direction came early this year when the government established two centres of excellence to study carbon removal. After a period of relative silence, early July saw a panel comprising representatives from the petroleum ministry, industry executives and academics putting forth a draft roadmap for carbon capture, utilisation and storage (CCUS) for upstream exploration and production companies. The roadmap aims to capitalise on “a once-in-a-generation opportunity to emerge as a global CCUS innovation hub.”

The opportunity referred to in the document is the climate crisis. Averting the crisis, according to the IPCC, would require a rapid expansion of carbon removal capacities in order to lower atmospheric carbon concentrations. In order to keep warming within a 1.5˚C temperature rise by 2100, the world will need carbon removal in the long run and rapid decarbonisation in the short term, according to the latest assessment by the IPCC. Models included in the 6th Assessment Report suggest that carbon dioxide removal (CDR) could rise to 6 billion tonnes of CO₂ (tCO₂) a year by 2050 under certain assumptions. Assessments done by the IEA, which considers the possibility of achieving carbon neutrality by 2050 while still accommodating an expanding carbon budget, show that the world needs to pull out nearly a billion tonnes of CO2 from the atmosphere every year. As of 2021, less than 10,000 tCO2 has been permanently removed. Without the flow of capital into CCUS, however, the cost of mitigation, according to the IPCC, is likely to more than double.

The urgency to remove carbon, along with the evolution of carbon pricing, emissions trading and increasing pressure on companies to declare emissions reduction plans has resulted in billions of dollars of private and public capital pouring into carbon removal technologies and companies. Several large investment groups, including the Amazon Climate Pledge Fund, Bill Gates’ Breakthrough Energy Ventures and even government agencies like the US Department of Energy are supporting the two broad categories of CCS: one that is applied to power plants and industrial facilities, and direct-air-capture (DAC). Both categories involve four distinct steps, namely, CO2 capture from anthropogenic sources compression, transportation, utilisation and storage, each of which can be resource- and energy-intensive.

The former captures carbon through chemical processes before it is released out into the air, and the latter sucks carbon out of the air (again through chemical agents) to ultimately achieve net negative emissions. The captured CO2 is dealt with in two ways: a) it is pumped and stored underground in abandoned oil and gas fields or rock formations that are judged to not be vulnerable to seismic activity, or b) it is repurposed for use with existing materials. The latter has spurred incredible innovation (more on that later) and is helped in no small measure by generous incentives, such as the $100 million XPrize Carbon Removal fund, supported by the Musk Foundation.

Bloated costs of capturing carbon

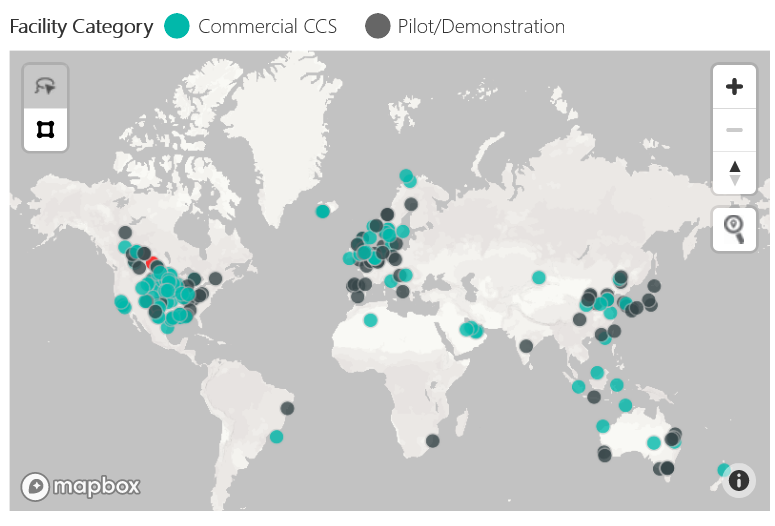

There are currently 59 CCS plants in service around the world that are together removing more than 40 million tonnes of CO2 every year. For context, the world emitted 43 billion tonnes of CO2, or a 1,000 times more than the removal capacity, in 2019. While two plants, both in the US, have also suspended operations due to accidents and poor economic output, there are reportedly around 75 plants at various stages of development and planning. One recent addition to the list of operating plants is the Orca direct air capture and storage plant in Iceland. Developed by Switzerland-based Climeworks, the plant will mix the CO2 with water and pipe it deep into underground basalt formations, where over time it will cool and turn into solid rock. Orca is rated to extract 4,000 metric tonnes (MT) of CO2 every year, but at $600-800/tonne of CO2 removal, its prices are prohibitively expensive.

Analysts suggest that they need to come down to around $100-150/tonne for such plants to turn a profit without any government subsidies. Climeworks co-founder Christoph Gebald says that is the target beyond 2030, after dropping to $200-300/tonne by the end of the decade as economies of scale kick in with additional units. He also points out that the state of California subsidises EVs to the tune of $450-500 per tonne of CO2 emissions (saved over their lifetimes), and this kind of the support would certainly be welcomed by CCS operators. But for now, customers that cannot afford to cap their own emissions, such as large industrial facilities, can pay Climeworks to do the job for them. In comparison, trees are estimated to perform the same function at a cost of about $50/tco2.

Except that Orca is blessed with access to Iceland’s cheap and zero-carbon geothermal energy, as well as plentiful water for the CO2 to be mixed with and just the right geological underbelly. In fact, that’s precisely why it was installed in Iceland. If it were to be set up in a water-stressed region (like most developing nations with coal plants) and the power for it came from fossil sources, the operation may end up releasing more CO2 than it absorbs (depending upon the plant’s efficiency) and worsen the local water availability.

Carbon Removal Technology is Scaling

CCUS technology is definitely scaling, even if far from the required rates, with the oil-dependent Middle East emerging as the hot new market. Oman and Saudi Arabia are the first in the region to declare their carbon-capture ambitions. The technology, too, has been diversifying, with new concepts to capture and store ocean-dissolved carbon being introduced into the commercial carbon removal landscape.

Still, atmospheric carbon capture remains the predominant mode. The Carbon Engineering-run plants in Texas, US, and Alberta, Canada, are much larger than the Orca at around 10,000 tonnes of CO2 removal capacity per year. The world would need nearly 21,500 such plants to reach the 6 billion tCO2 figure included in the IPCC assessment. To achieve net-zero status by 2050, the number of such plants would need to be closer to 100,000. Even conservative estimates would put the required capital expenditure at several hundreds of billions of dollars and aggressive carbon pricing regimes to sustain.

The utilisation of sequestered carbon is slowly but surely emerging as an option to increase the circularity of carbon and extend its value chain. Spurred on by the XPrize challenge, a number of brilliant minds have devised uses for the captured carbon that have birthed an entirely new industry: carbon-based consumer goods. The products include diamonds and high-end sportswear, carbon sunglasses, shampoo bottles and wallets, and the idea behind “carbon recycling” is to make CCS (much) more remunerative by creating mass market demand for carbon. Also, the two winners of the XPrize Carbon Removal challenge—they will receive $7.5 million each—will capture CO2 from a coal and natural gas plant (in Wyoming and Alberta, respectively) and inject it into concrete in a manner that will lower the manufacturers’ water requirement by up to 50%, and add to the material strength of the concrete. Concrete is one of the most abundantly used manmade materials and accounts for roughly 8% of global CO2 emissions, so the advancements would be a big step towards sustainable construction.

Captured carbon can also be applied to agriculture, to improve soil carbon and spur plant growth. Australia-based Global CCS Institute suggests that this application makes CCUS a useful piece of the Just Transition puzzle as the world looks to tackle emissions from agriculture as well as the looming food security question. It says that instead of the renewables-related manufacturing jobs migrating to a few production centres (mainly China), CCS could create high-value jobs in virtually every country and avoid the socio-economic shut down costs of retiring existing fossil fuel capacities. From 40 million tonnes per annum at the moment to an estimated 5,635 MTPA of CO2 removal by 2050, expanding CCS facilities may certainly require much more manpower.

India’s Carbon Sequestration Roadmap

India, which emits about 2.65 GT of CO2 annually or 7% of the global total, is the world’s third-largest emitter of CO2 emissions after China (28%) and USA (15%). Over two-thirds of the country’s emissions can be attributed to the energy sector and while India’s per capita emissions continue to remain far below the average in developed economies, international pressure to ratchet up its emissions reduction ambitions have been increasing in recent years. The 2070 net-zero target announced last year includes short-term targets of reducing projected carbon emissions by 1 billion tonnes by 2030 and bringing down the carbon intensity of the Indian economy by 45% by 2030 relative to 2005 levels.

India’s recently released draft roadmap primarily focuses on emissions removals from fossil fuel energy projects. Although the draft lists four separate methods of CDR, it predominantly covers post-combustion carbon capture on site, given the relative ease of retrofitting the required technologies. The draft advocates for the recovery and transport of carbon to be then injected into oil producing reservoirs for enhanced oil recovery (EOR). Even though a majority of global CCUS projects utilise removed carbon for similar purposes, the draft goes on to acknowledge that given the spatial and geographical limitations of oil and gas fields, there is a possibility that future CCUS projects will shift to permanent geological storage, in which the carbon is injected into cracks and fissures of suitable geological bedrocks.

The draft identifies four distinct methods with significant storage potential in the country— storage through CO2 enhanced oil recovery (EOR), enhanced coal bed methane recovery (ECBMR), in deep saline aquifers, and basalt formations. While the first two are methods to plug carbon right back into fossil fuel production channels, the latter two involve permanent geological storage.

Estimates included in the draft show a viable capacity of 1.204 GTCO2 in India’s oil and gas fields and storage capacity between 3.5-6.3 GTCO2 in the country’s coal reservoirs. Saline aquifer and basalt storage are estimated to be around 291 GTCO2 and between 97-316 GTCO2 respectively. While acknowledging the high costs of CCUS and the risks associated with transporting sequestered carbon, the draft goes on to advocate incentivising CCUS through direct capital gains, subsidies, carbon pricing, prioritising procurement of low-carbon products and support for R&D.

Currently, there are no active operational CCUS plants in the country. The first one to come online will likely beat IOCL’s Koyali refinery. The project envisages piping captured CO2 from the refinery to ONGC’s Western onshore field in Gandhar about 80kms away where it will then be used for EOR. Oil India Limited’s (OIL) Naharkatia Oilfield in Assam has also been identified as a candidate for CO2 utilisation for EOR.

Big players in India’s private sector have been moving too, to insert themselves into the country’s nascent captured carbon value chain. Dalmia Cement’s Ariyalur plant in Tamil Nadu, which requires a total of 5 MTPA of coal for production and also has a 27MW captive power plant for electricity, recently conducted a feasibility study for carbon capture and utilisation for urea production with the help of the Asian Development Bank. According to the feasibility report, viable CCU integration would be along with a biomass boiler and fossil fuel-based ammonia, which could reduce CO2 emissions from the plant by about 60%. This, however, would come at a cost of $2.9 billion, just to set up the plant alone.

For a base case where 0.5 million tonnes of CO2 is converted into 680,000 tonnes of urea, the capital expenditure (CAPEX) for the project is estimated at $365.43 million (Rs26,417.98 million) or $730.86 (Rs52,835.96) per tonne of CO2 for conversion into urea. Operational Expenditure (OPEX) for the conversion is determined as $167.35 million (Rs12,098.23 million) or $316.34 (Rs22,869.17) per tonne of CO2 converted to urea, including capture cost is $55.65 per tonne. The requisite price of carbon credits to achieve a 20% internal rate of return has been estimated to be around $85/tCO2. Other estimates have pegged the carbon pricing to be around $57-68/tCO2 for CCUS to become viable in India. If passed on to the end-consumer, this additional cost could have an amplified effect on economic demand. While costs have been prohibitively high, it has not stopped other Indian businesses from incorporating CCUS in their long-term decarbonisation strategies, most notably steel companies such as Tata Steel and JSW.

Claims aplenty, low accountability on CO2 capture

While economic and natural resource feasibility continue to dog the prospects of carbon capture, utilisation and storage, activists have also pointed to the lack of evidence of real world emission reductions from carbon removal projects. A recent report by Transparency International pointed to the lack of any clear regulations or multilateral governance or verification process to flag risks of corruption, lobbying and unverified claims emerging in the CDR landscape.

Additionally, activists have also propped up the notion that expanding CCS would in effect prolong the use of fossil fuels. Indeed, the oil and gas industry has been one of its strongest supporters, not just because the captured carbon (CO2) can be piped down into underground deposits to extract even more oil—a process known as Enhanced Oil Recovery. It can extract up to 60% of a reserve’s oil deposits—some studies say it could boost oil output from deep beneath the North Sea by 15%—but is different from fracking in that it scrapes the rock formations and does not crack them open. It is widely used across North America, but one would argue that CCS overall obviates the need to throttle emissions and switch to clean alternatives. Further, transportation and storage of removed carbon open up risks of leakages and environmental contamination. Natural gas pipelines, which are responsible for a large chunk of the associated fugitive methane emissions stand as evidence of these risks.

There is merit to the argument as it is not just the carbon footprint of the fossil fuels industry that needs to be managed, but also its ecological and public health impacts. The Deepwater Horizon spill in 2010 released 210 million gallons of crude oil and is expected to disrupt marine life and contaminate the food chain in the Gulf of Mexico for generations. Also, as the Arctic ice cap thaws and Big Oil looks to move in, the spectre of an oil spill in the pristine waters is a very real possibility.

While removal and utilisation of CO2, at least in theory, offers a way to reduce the burden of carbon, governments must be wary of substituting the need to cut-down on fossil fuels with a still contentious and incredibly expensive technology. While a measured approach to CCUS could indeed evolve into a win-win situation that delivers emissions reductions and economic benefits, as has been claimed by proponents, over-reliance on these methods and low accountability could very easily turn this hail Mary into a lose-lose.