A green taxonomy will help India attract more green finance for its ambitious climate actions, but it must also be wary of pitfalls that plague taxonomies in other geographies, say experts

The latest IPCC working group report on mitigation has listed out the need to cut global emissions as soon as the world can and the ways to do it. Although developed countries cutting their emissions quickly is a more effective solution, an ongoing flattening of historic responsibilities is piling pressure on developing countries like India to ramp up climate action as well.

Underpinning these developments, however, are billions of dollars that are needed in emerging economies to take on that challenge. While developed countries keep under-delivering on their commitment to provide $100 billion a year in climate finance to the developing world, which itself is a drop in the bucket as far as needs go, there has been a clear shift towards private finance when talking about delivering climate action.

Under pressure to relinquish their claim on international public finance for climate action, tapping into private capital is critical for large developing countries like India, experts say. In order to manage the risk perception of a developing economy and an under-developed financial market, India desperately needs a document that would standardise the definition of green and map the segment in its economy where green investments are possible. In other words, India needs clearly defined rules of engagement that would ideally help drive investment decisions towards sustainability and progressive climate action. A few countries, including the European Union (EU), China and Malaysia, have already developed such documents, loosely called ‘green taxonomies’.

Under a larger framework of sustainable financial architecture, a task force established by India’s finance ministry is working to develop such a taxonomy. However, no information regarding this document has been made public, so far. Sources privy to the discussion said that this taxonomy might not exclusively address “green finance” but the larger segment of “sustainable finance” which subsumes green segments as well.

As India prepares to come out with its macro-view sustainable finance taxonomy, there are some lessons from other ‘green taxonomies’ and economic trends from around the world that India needs to be cautious of.

Why is a taxonomy important?

The lack of clarity surrounding India’s sustainable finance and the rules that govern them has meant that the country has so far been unable to tap into the pool of international green finance in any major way. A Climate Policy Initiative report from 2020 highlighted that green finance investments for the financial years of 2017 and 2018 in India were only 10% of the total required investment of US$ 170 billion per year. The share of international private finance was just 5% of tracked domestic green finance.

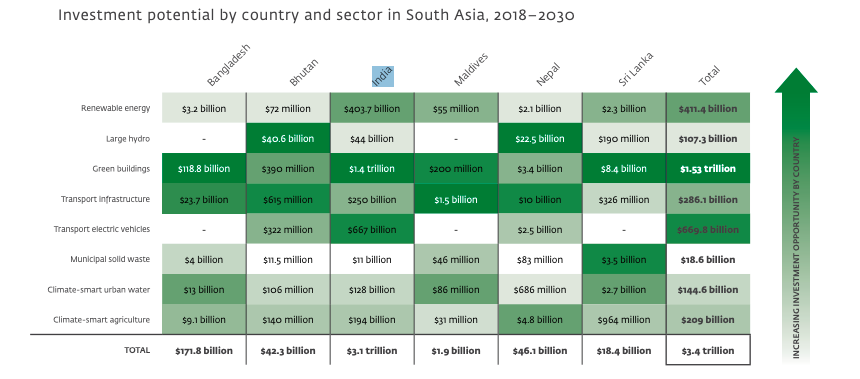

As for the potential, The International Finance Corporation (IFC) has estimated that India has a climate-smart investment potential of $3.1 trillion from 2018 to 2030. The largest space for investment is in electric-vehicle segment, at $667 billion as India wants to electrify all of its new vehicle by 2030. India’s renewable energy sector, steadily, continues to be a good investment avenue at $403.7 billion. (See the chart below)

This is the money that India cannot afford to miss given the ambitious goal it has set for itself. At the 26th Conference of Parties (COP26), Indian Prime Minister Narendra Modi declared a five-pronged “panchamrit” strategy reliant heavily on transformational changes in India’s energy systems to take India to net zero by 2070.

“These targets represent a roadmap for India’s green transition. A transition that represents a new type of growth and a major overhaul of the existing systems of production. It will also demand significant investments,” says Renita D’Souza, fellow, Observer Research Foundation, a New-Delhi-based think-tank.

“It is very important, therefore, for India to standardise what is green and establish the eligibility criteria for green finance. As such, a green taxonomy is critical at this juncture for India,” D’souza told CarbonCopy. “It will help garner the finance that this massive transition needs,” she adds.

Even if India comes out with a larger sustainable finance taxonomy instead of a more granular one that defines green, it will still be very helpful at this stage for the country to streamline the information asymmetry.

A sustainable finance taxonomy is a classification system, with specific performance thresholds, that defines what constitutes a sustainable activity. It provides a common language for equity investors, lenders, policymakers and regulators to clearly identify the economic activities that contribute to a country’s sustainability priorities, says Arjun Dutt, an expert on green finance working with the policy think-tank, The Council on Energy, Environment and Water (CEEW).

Such a system mitigates the risk of greenwashing and facilitates the linking of sustainability investors with credible sustainable investment opportunities. It can also provide the basis for redesigning policy and market incentive structures to align investments with sustainability as well as a basis to track these investment flows, Dutt adds.

What are the challenges?

There is little doubt that how far India (or any other country) can realise its climate ambition will depend heavily on how much money is available and accessible for individual objectives. As far as the economics of climate action goes, capital is king. While negotiators press on with demands to keep the principles of historic responsibility, equity and common but differentiated responsibilities (CBDR) front and centre in matters of international public climate finance, hoping for these funds to not only transpire but also be adequate to power economy-wide climate action is a dangerously foolish gambit.

India’s domestic sources for green finance are still limited, as the CPI report shows. But, according to D’Souza, there is enough money available for green actions from international sources—a collective Asset Under Management (AUM) of $81.7 trillion under the 1,715 signatories to the Principles for Responsible Investment as of April 2018; some 534 sustainability indexed funds overseeing a combined $250 billion as of the end of the second quarter of 2020, and the impact investment market worth $715 billion.

But why does global private finance, so far, only form a fraction (5%) of India’s already meagre flows of total green finance?

The lack of definition of what activities can be deemed green is a massive impediment. Then there are the traditional risks of investing money in a low-middle income economy that is still developing, India’s government think-tank, Niti Aayog’s CEO Amitabh Kant and researcher Sweety Pandey wrote in an article, “This can dent the integrity of the market and increase the risk of damaging investor perception and demand.”

A green taxonomy, as per D’Souza, will help tackle most of these challenges by providing a standard definition of ‘green’ along with a rulebook “for determining the eligibility of economic activities/projects/assets for such finance.” In addition, a green taxonomy will also help the country deal with its non-coherent publishing of green finance data by minimising information asymmetry, which would also increase investor confidence.

By delineating the eligible economic activities, it will help financial institutions understand the investment peculiarities of green projects and leverage financial innovations accordingly, D’Souza adds.

About 80% of India’s green finance is being used to build the country’s renewable capacity.

Dutt of CEEW says a proper taxonomy will provide visibility to other sectors in need of investment that remain starved of capital. “The inclusion of market segments, including those that are financially underserved, in a sustainable finance taxonomy is a policy signal for investors to direct capital flows towards them. Designing policy and market mechanisms that de-risk investments in financially underserved segments that have not attained commercial viability could accelerate capital flows towards them.”

Extending the taxonomy to include transition segments could further help identify the conditions under which investments in these segments are aligned with economy-wide decarbonisation trajectories. This could help channel capital flows that finance these hard-to-abate sectors to the extent that they support economy-wide decarbonisation, Dutt explains.

Some of the examples of these transition segments could be a cement plant looking to go green, transmission assets which carry both green and brown electricity or distributed renewable energy applications like a solar-powered coal storage facility or solar-powered textile facility or a flour mill.

The biggest benefactor of visibility through a taxonomy could also be India’s cash-strapped adaptation actions.

“Mitigation has always been considered measurable, whereas adaptation is typically perceived to be too complicated to measure,” Namrata Ginoya, programme manager – energy and resilience with World Resources Institute, India, tells CarbonCopy.

“Scientists, policy researchers and economists have shown through various studies that it is possible to measure adaptation gains. However, these studies have either failed to bring the conventional finance sector into the fold or they are focusing on the perceived quick gains with the mitigation sector.”

The task is not so simple, D’Souza of ORF warns. Climate adaptation is location and context specific. Developing a taxonomy for it is not as straightforward as for mitigation, she says. And if such a taxonomy is successfully developed, she adds, that it will have identified basic principles that would determine whether a particular activity can be regarded as climate adaptation or not. This would solve the most fundamental challenge of greenwashing in the context of climate adaptation.

Russia, Mongolia, Malaysia, China and the EU have their taxonomies in place. What are the learning that India can take from these taxonomies?

The China, Mongolia, and EU taxonomies concur on the need to identify sectors that can deliver significant positive impacts across environmental objectives. The China and Mongolia taxonomies further observe the importance of timely updates according to changing needs. In the context of screening criteria, the Mongolia, Egypt and EU taxonomies are important, since they address the specific needs of the geographies that they attend to.

The differences in the screening criteria reflect the need to cater to national/ regional circumstances and adhere to national/regional standards and norms. Unlike the Bangladesh, Malaysia and China taxonomies, the Indian taxonomy must establish appropriate screening criteria to reflect domestic realities and align with national standards/norms.

The Mongolia, Malaysia and EU taxonomies cater not only to banks, financial institutions and investors, but also to companies, project developers, credit-rating agencies and standard setters. This is indicative of the utility and contribution to the development of the broader green finance ecosystem. The Indian taxonomy must be formulated in a way that gives direction to the development of its green finance ecosystem.

The EU iteration is the most comprehensive and sophisticated template of a regional/national taxonomy, anchored in scientific evidence, and can be modified to accommodate specific regional/national concerns without losing the essence of the template. The clarity and the detail afforded by this taxonomy makes it the top choice as a reference framework. For climate mitigation, the document prescribes technology agnostic metrics and thresholds to define eligibility for green finance.

– Renita D’souza, Fellow, Observer Research Foundation (ORF)

A taxonomy is as strong as the environmental process it is built on

For a green taxonomy to be robust and increase the confidence of International players in India’s green finance sector, there are some precautions that need to be considered. First, gauging the strength of India’s existing green laws and second, considering the mistakes in other countries’ taxonomy journeys.

Of late, the Indian government has been facing criticism for systematically diluting the country’s laws, including those on its forests, biological diversity, coasts, pollution norms and rights of people at the intersections, to promote an easy atmosphere for industries, as media reports show. This could weaken the strength of India’s green taxonomy that will be heavily informed by these rules.

“The green taxonomy’s eligibility criteria ought to be anchored in the environmental norms and standards of the country. Hence, compliance with the taxonomy is underpinned by these environmental norms. Diluting them will definitely undermine a robust taxonomy,” D’Souza says.

According to Dutt, best practices pertaining to eligibility criteria in taxonomies entail simultaneously ensuring positive contributions to specific environmental objectives without compromising on others.

For example, Dutt elaborates, “the EU Taxonomy requires eligible activities to have a “substantial contribution” in advancing one environmental objective while ensuring activities do no significant harm to other environmental objectives.”

If an Indian taxonomy follows similar principles, it could ensure that eligible activities result in an overall positive impact from the perspective of sustainability, he adds.

India’s green taxonomy discussion should also draw information from debates happening around the world about the EU’s latest proposals regarding its taxonomy. The European Commission, this February, announced a proposal to include “specific nuclear and gas energy activities” in the EU taxonomy for sustainable activities to meet its 2030 climate targets. It underscores the role of gas as a transitional fuel to move from coal to renewables and sets out certain conditions under which construction of gas infrastructure would be allowed. But this has drawn serious criticism given its dissonance with climate science—both IPCC recommendations and the EU’s own stated goal of net-zero by 2050. Criticising this, scientists, civil society groups, and even financial institutions said, “the taxonomy itself would become a greenwashing tool” given the warming potential of methane, CarbonCopy reported on March 21, 2022.

As India explores green/low-carbon hydrogen and other transitional fuels like gas, it could try and avoid similar mistakes. However, beyond science, politics around global energy supply chains will have a clear influence over what India decides to include in its green taxonomy.

Transition segments, according to Dutt, should be included conditional on strict criteria that ensure that these are aligned with long-term decarbonisation trajectories. For example, the proposed inclusion of gas in the EU Taxonomy also entails the requirement for facilities to switch fully to renewables or low-carbon gases by 31 December 2035.

“Similarly, India could consider including both low-carbon and transition segments when developing its taxonomy to the extent that these are consistent with the ambition of net-zero emissions by 2070 or a more ambitious target set by policymakers for the country in the future,” Dutt added.

But India needs to be careful

Former chief economic advisor to the Indian government, Arvind Subramanian, in a January 2020 column, warned against a future reality if India fails to deal with the fuzziness of sustainable finance regulations. If trillions of dollars in climate finance go to emerging markets, the flows could amount to 5-10% of these economies’ GDP — similar to the financing surges that preceded the 1997 Asian financial crisis and the 2013 ‘taper tantrum’. Unregulated private capital flows of this magnitude will lead to overheating, volatility, imprudent lending, and overvalued exchange rates. Speaking of the elephant in the sustainable finance room- ESG funds, Subramanian wrote that eventually, when the mania is seen for what it is, costly consequences will follow: capital flows will reverse, and both output and the financial sector will collapse, he wrote. A rise in interest rates in developed economies could make the capital costly and inaccessible for developing countries, but currently “enough liquidity still sloshing around in the system” is making the risks connected with large ESG flows and climate finance real, he wrote.

“The halo of perceived social good” along with the impression of ESG funds being less risky, “could easily lull regulators into leniency and inattention,” per Subramanian.

Through a “cynical view” he warned that the “private climate finance could end up damaging poorer economies and producing little by way of climate-positive outcomes, while enabling the financial sector to coat its somewhat tarnished reputation with a patina of green.”

About The Author

You may also like

India’s EV revolution: Are e-rickshaws leading the charge or stalling it?

Is pine the real ‘villain’ in the Uttarakhand forest fire saga?

NCQG’s new challenge: Show us the money

India’s energy sector: Ten years of progress, but in fits and starts

9 years after launch, India’s solar skill training scheme yet to find its place in the sun