A slew of protectionist measures in response to soaring food prices by several major exporters has raised alarm bells over food security in the short term. In the longer term, it raises questions of how food security priorities can be aligned with those of effective climate action

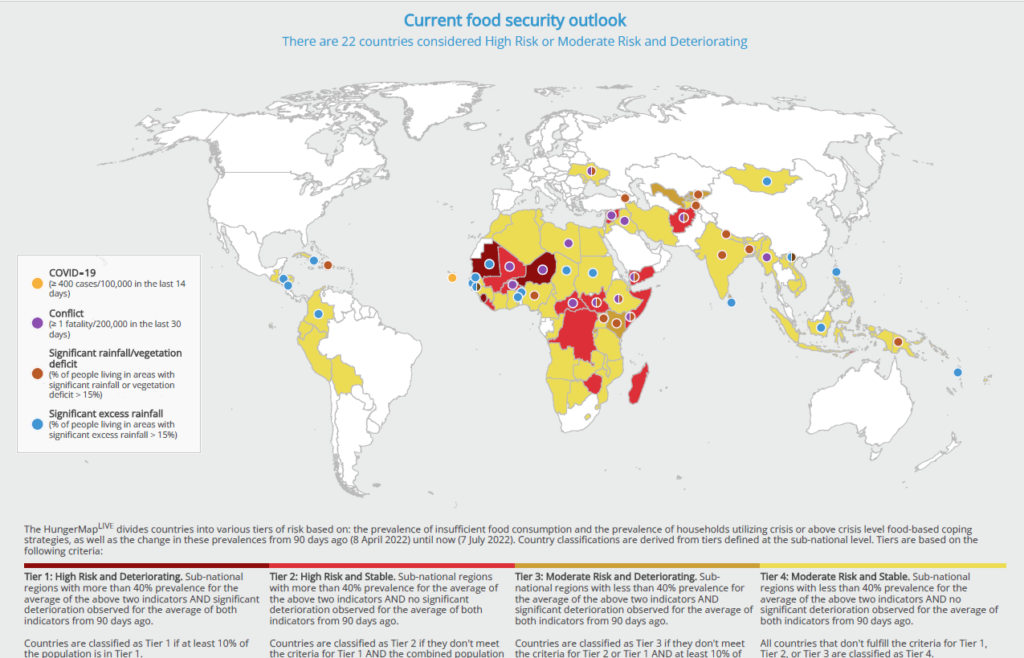

The global pandemic in 2020 has triggered a food and nutrition crisis that has continually gotten worse and is fuelling dangerous levels of insecurity. This is the key takeaway of the UN State of Food Security and Nutrition report published on July 6. The number of people affected by hunger grew sharply by over 22% compared to pre-pandemic numbers to 828 million people in 2021. Following a period of relative stability between 2015 and 2019, the proportion of the global population jumped by 1.8 percentage points from 8% to 9.8% between 2019 and 2021. Meanwhile, nearly 30% of the world or 2.3 billion people recorded at least moderate food insecurity, an increase of nearly 350 million people since the outbreak of COVID-19.

The situation only seems to be getting more dire in 2022, with the World Food Program estimating the number of people currently enduring insufficiency of food at 871 million across 91 (mainly developing) countries. The surge in food insecurity has come alongside protracted increases in food prices since the beginning of the pandemic.

The UN Food and Agriculture Organisation (FAO) revealed in its March update that food prices had increased by a whopping 70% since mid-2020. A more recent estimate of the increase in food prices comes from the World Bank’s Agricultural Price Index, which has registered a hike of over 34% as of June 30, 2022 as compared to January 2021. Heading into the second half of the year, more warnings have ensued that given the spike in input costs, directly affected by higher energy prices and supply chain disruptions emanating from Russia’s “special military operation” in Ukraine, there could be further elevation in food prices during the remainder of 2022.

How climate change is making a bad situation worse

Climate change will increasingly be detrimental to crop productivity as levels of warming progress—the IPCC made this high confidence statement back in 2019. The sentiment was emphasised again in 2021 and 2022 in the second and third instalments of the IPCC’s Sixth Assessment Report.

Over the past few years, the impacts of climate and extreme weather on India on agricultural and food commodity prices seem to have crystallised like never before. India, for example, recorded its hottest March in 122 years this year, the direct result of which was a significant drop in wheat yield. India was to increase its wheat production to help ease the global shortage of the crop after the invasion of Ukraine, which is a major supplier to the west. Similar fears have now surrounded India’s rice yield for the year after a staggered onset of the monsoon has delayed sowing in several parts of the country.

But climate-change-induced heatwaves forced India to ban exports of wheat in May this year in order to provide enough domestically. The ban on wheat followed similar restrictions on sugarcane exports. India is not the only country to have a protectionist response to the food crisis. Indonesia banned palm oil exports, while China restricted its global supply of fertilisers following the Russian invasion. Malaysia last month announced an export ban on chicken this week amid fears of domestic shortages. Piling export restrictions, particularly in major agricultural hubs, prompted the WTO to issue a warning of the dangerous implications of continuing such bans.

The rise in fertiliser and other input prices have added to soaring food costs, which have been taking a toll on food security and nutrition even in developed parts of the world, including the US, UK, Europe and Australia, from which they have typically remained insulated. The continuation of a multi-year protracted drought in several parts of Africa has further heightened the risks of food insecurity, especially in import-dependent countries already reeling from record high food prices and disrupted supply chains.

Extreme weather, pest attacks and crop diseases that have plagued global agricultural output in recent times have all been linked to climate change. What doesn’t help matters is that global food production of essential crops is concentrated in a small number of countries that are especially vulnerable to the effects of climate change.

Regions that are not exposed to such extreme events, but depend on food imports, are also, therefore, indirectly affected. In other words, we are all in this together, even if the degree of impact varies. Even the IPCC, in its latest report on adaptation, emphasised on international cooperation as an important tool for effective climate action.

The third wave of protectionism

Sadly, the exact opposite is evident from government responses to the string of recent crises. After nearly three decades of seemingly unstoppable globalisation across economic value chains, the outbreak of the COVID-19 pandemic has exposed the fragilities of global supply chains. The pandemic itself set off the first wave of protectionism as governments sought to control vaccine technology and supply chains while pushing for global mandates. The rollercoaster in energy markets through the lockdowns, the recovery and the conflict in Ukraine has spurred growing protectionism in energy. Food and agricultural commodities over the past few months have now carried the third wave of protectionism in the last two years.

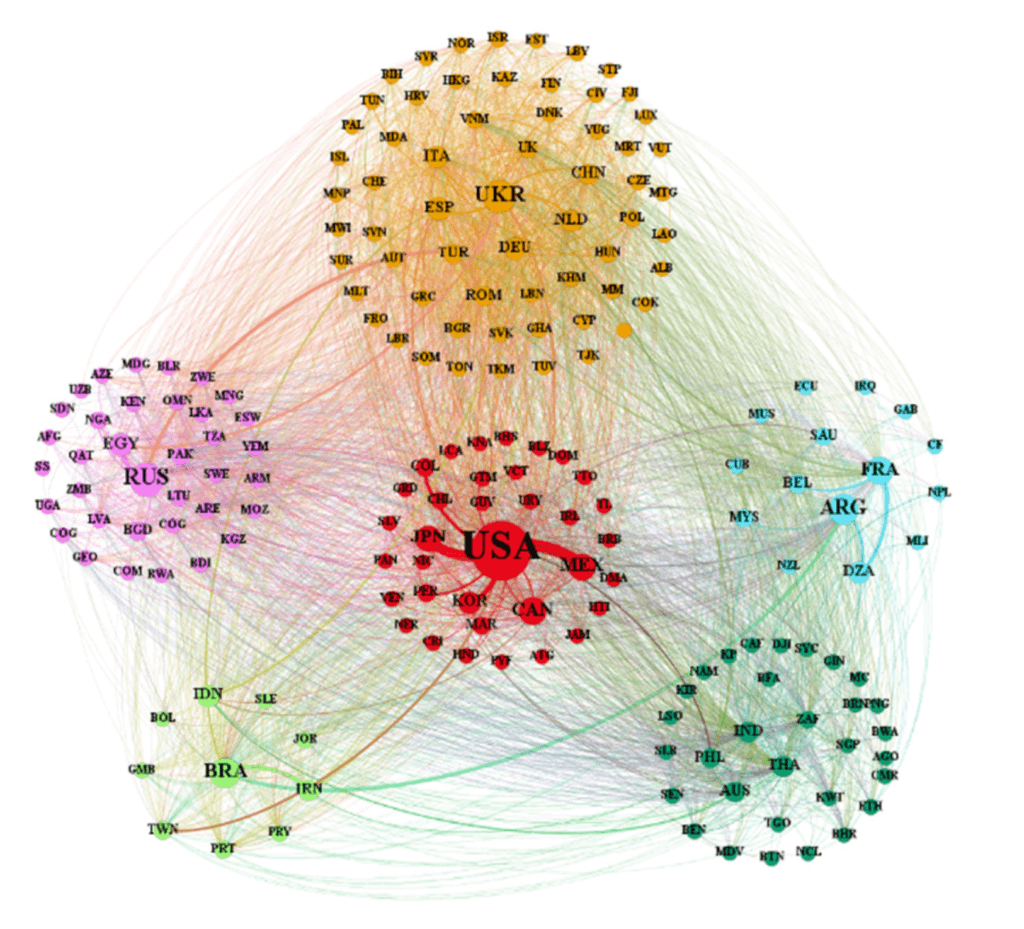

Although food supply chains have become substantially more dispersed in the post-Cold War era, supplies have remained fairly concentrated. Network analysis conducted on global food trade patterns published in 2021 by the Chinese Academy of Sciences shows that the food trade network has evolved from unipolar to multipolar.

While major food producers have changed since 1992 and more countries have emerged export hubs, 80% of all food exports still come from just 10 countries. At the same time, the imports have shown increases in both the number of recipient countries and extent of dependence. Interestingly, Ukraine and Russia replaced other major European agricultural producers following the end of the Cold War to become major suppliers of multiple food staples and agricultural inputs to the global market. The conflict in Ukraine and trade sanctions on Russia that have followed have effectively curbed one of the most export hubs in global food trade, widespread effects on supplies, prices and food security across the world.

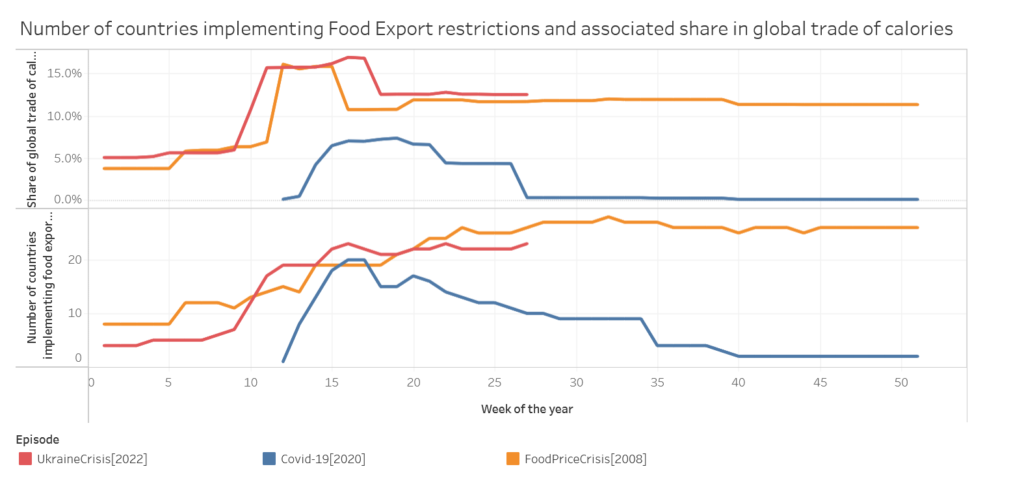

According to the Food and Fertilizer Export Restrictions Tracker maintained by IFPRI, export limitations at the height of restrictions in April-May this year accounted for almost 17% of global trade of calories from 23 countries, including some major cogs in global agricultural supply chains like India, Indonesia, Argentina, Turkey and Russia. Another eight countries have introduced new export licensing measures.

As far as fertilisers go, current restrictions affect over 20% of global supplies of all major categories (nitrogenous, phosphates and potash). Current levels of restrictions have not been seen since the 2008 food crisis that set off several conflicts and food riots around the world. The current food crisis, however, is compounded by a cocktail of ominous developments in the geopolitical arena and an aggressively inflationary environment following stimulative spending undertaken to keep the global economy afloat during the pandemic.

Under the current set of geopolitical and economic variables, food is fast becoming the new oil. India, for example, has decided to permit the export of wheat to Indonesia in exchange for the latter’s palm oil. These export restrictions and government-to-government deals, however, offer a myopic solution to a problem that transcends borders, and have disproportionate impacts on the world’s poorest and most vulnerable.

The seen and the unseen

Global food prices are unlikely to stabilise with such short-term measures. Import-dependent countries such as those in Africa are already getting the short end of the stick, as are low-income households in developed countries. The surge in food prices due to protectionist measures affects all food importing countries, but also exacerbates inequality between and within countries as well. While rich countries and populations can afford to keep buying the high prices, populations in poorer economies are priced out and forced into dietary compromises. Within these countries, low-income households and other vulnerable groups like women, children and the elderly bear a disproportionate brunt of price escalations and limited access.

The past month has seen energy prices come down due to a surging dollar and forecasts of recession-led demand downturns and export restrictions have slightly loosened as well. They, however, remain well above pre-pandemic levels and hyper-sensitive to developments in geopolitics, energy prices, supply chain disruptions, and the impacts of unfavourable weather. A recession, which seems all but confirmed at present, will likely keep food markets tight if not make them worse.

The frailties in global food supply chains have been laid bare multiple times since the COVID-19 pandemic. While calls for collaborative action to alleviate the global food crisis have been raised at multiple inter-governmental platforms, a natural response in many import-dependent countries, particularly in Africa and Asia, has been to prioritise food security. With the effects of climate change only likely to strain global food supply chains, meeting the objective of food security could see widespread changes in land use and more land coming under cultivation. Will this lead to an expansion and deepening of the environmental imprints and carbon footprints?

Overseas development aid has increasingly been aligned with food security, evidenced by the $5 billion pledge made towards global food security by G7 countries. So has private capital, as was clear at the World Economic Forum in Davos in May where the combination of food security and climate concerns culminated in the resurgence of the “climate friendly farming” lexicon. But the problem is far from being simple enough to solve by throwing money at it. With mega billionaires and investment giants showing massive interest in agricultural technology under the guise of climate change mitigation and adaptation, the world’s food shortage problem could well turn out to be yet another David versus Goliath battle.

This is the first in a series on the evolving food security crisis and how it intersects with the future of climate action

About The Author

You may also like

India’s EV revolution: Are e-rickshaws leading the charge or stalling it?

Is pine the real ‘villain’ in the Uttarakhand forest fire saga?

NCQG’s new challenge: Show us the money

India’s energy sector: Ten years of progress, but in fits and starts

9 years after launch, India’s solar skill training scheme yet to find its place in the sun